Does the concept of creating a budget overwhelm you? Does it cause you to worry that you will never be able to have fun again? Fear not! Contrary to what people may think, creating a budget is not meant to be stress-inducing. In fact, living within the budget you create for yourself can give you significantly more peace about your overall finances. Having a budget helps you to be in control of your money and to be more aware of where it is all going each month

First things first, there is not one budget strategy that is more “correct” than another, because when it comes to your hard earned money, it’s pretty easy to recognize that budgeting is actually quite personal. Everyone will do it a little bit differently. Budgeting methods are not one-size-fits-all, but there are a few things that every budget should accomplish for you. A good budget will enable you to pay for your needs, save for the future and emergencies, and it still leaves room for you to buy some of your additional desired things.

Two Types of Expenses

When we talk about expenses, it’s important to note that there are two types of expenses: fixed expenses and variable expenses. Fixed expenses are those which do not really change from month to month such as rent/mortgage, car payment, utilities, insurance, etc. Variable expenses are those which do fluctuate--groceries, entertainment, gas, and so on. Keep in mind that making cuts to your variable expenses is a really practical way to add some financial flexibility into your budget when money is tight. It’s really easy to underestimate your monthly expenses, so take the time to really figure out what your expenses truly amount to.

Budgeting Methods

1) 50-30-20 Budget Method

One of the most popular budgeting strategies is the 50-30-20 rule. In this plan, you allocate 50% of your income to your needs, 30% to your wants, and 20% to your savings/debt repayment.

For example: if your net pay each month is $3,500, under the 50-30-20 rule you would allocate $1,750 to necessities like rent, utilities, and other bills; $1,050 to your wants like eating out or shopping; and $700 to saving or debt repayment. Depending on your income it may be challenging to stick with these percentages exactly, but try to keep them as a close guide. If your needs each month equal more than 50% of your take home pay, make up the difference from your personal spending money rather than your savings/debt repayment money.

There are multiple budgeting styles out there and the 50-30-20 strategy is an example of a loose budget. It gives you the big picture for your finances without going into the small details. You can get as detailed as you want with your budget.

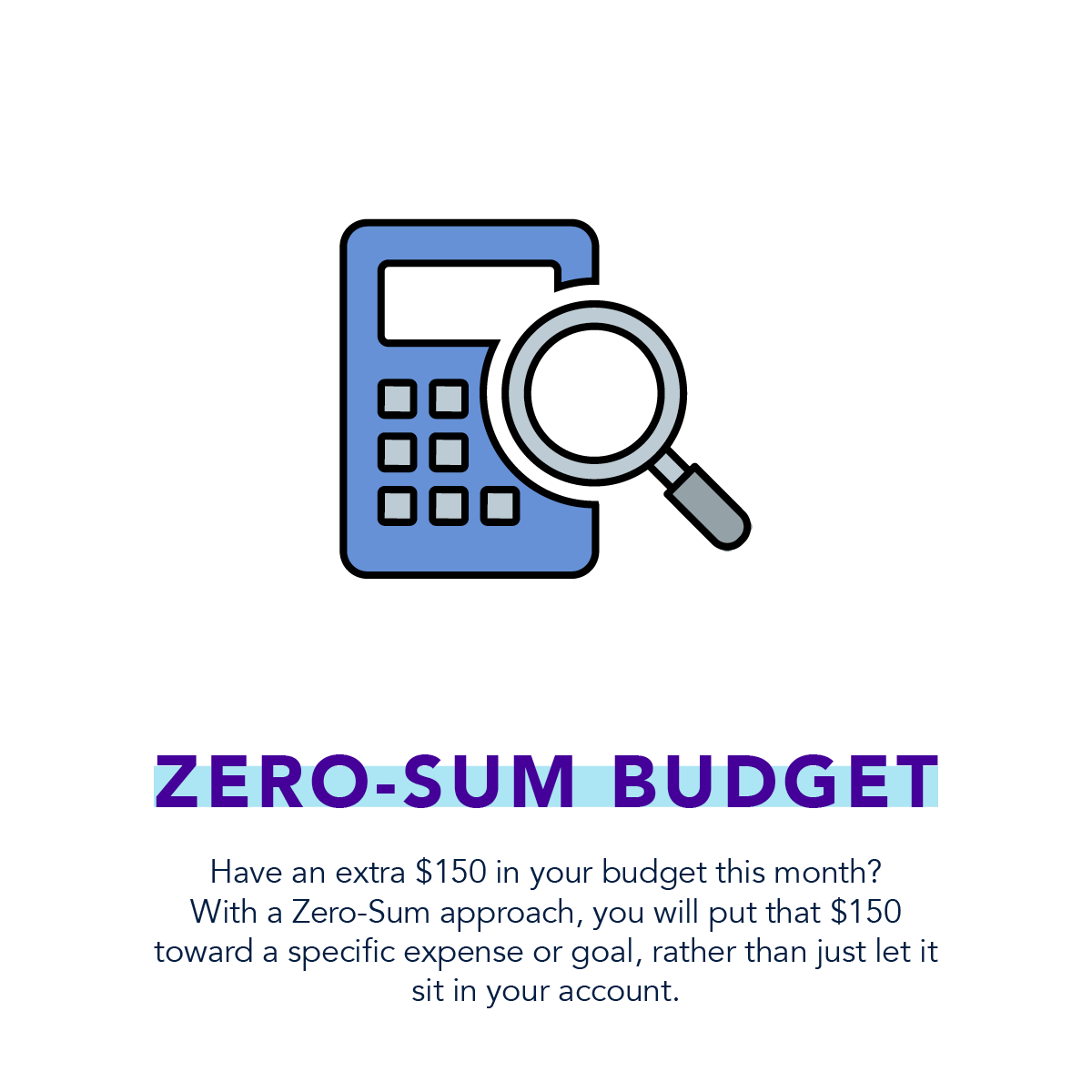

2) Zero-Sum Budget Method

A Zero-Sum budget is one in which you allocate every dollar of your budget, meaning that you start and end each month with $0, because even if you have extra money within the month, you allocate where it is going to go. Have an extra $150 in your budget this month? With a Zero-Sum approach, you will put that $150 toward a specific expense or goal, rather than just let it sit in your account.

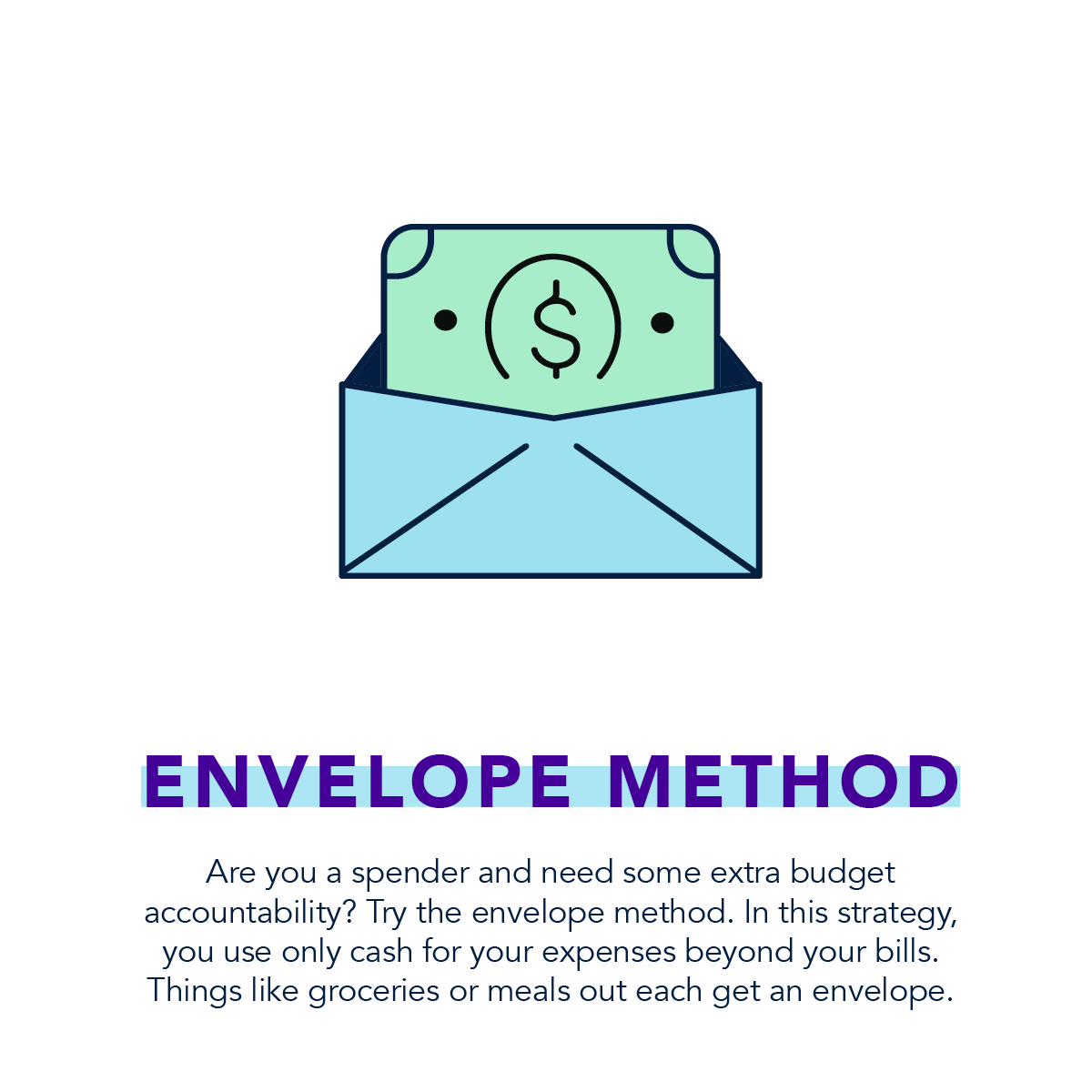

3) Envelope Method

Are you a spender and need some extra budget accountability? Try the envelope method. In this strategy, you use only cash for your expenses beyond your bills. Things like groceries or meals out each get an envelope. If your monthly budget for groceries is $175, you will not be able to spend any more of your cash on groceries once it runs out (unless you take the cash from one of your other envelopes). Using envelopes serves as a blatant visual reminder of your financial allotments and priorities. The envelope method can be a good way for you to get really honest with yourself about how much you are spending on different things, reallocating as needed, and practicing restraint.

4) Incidental Budget Method

Most of us have some familiarity with the concept of having an emergency savings fund as well as the importance of contributing to retirement savings, but there are always some special circumstances that pop up and demand your money, aren’t there? Try to allot some of your savings to an incidentals budget that will help you cover things like car repairs, home repairs, or other unexpected expenses. Additionally, you may want to adjust your budget seasonally, because throughout the year, your spending will have some natural ebbs and flows. A seasonal budget prepares for the extra expenses that come along with things like a summer vacation or the holiday season. If you know you will want to go on a summer vacation that will cost $1,500--save up for it throughout the year.

Keep Yourself Accountable - and Be Flexible

It’s highly unlikely that the first budget you create will be totally accurate. Budgets require some refinement over the course of time--both short term and long term. From the start, be honest with yourself about what your financial priorities are and figure out how to work with them. As you budget, and continue to tweak your budget, you will learn your priorities, re-prioritize, and experience shifts in your finances.

Keep track of your spending by using an app, creating your own spreadsheet, or just writing it out with a pen and paper. Do whatever works best for you. The ultimate goal of tracking your budget and spending is that you stay informed and accountable. Your budget will not feel overwhelming or tedious if you take a few minutes each day or week to assess where you are at with your monthly budget and if there are any adjustments you need to make.

Be flexible with your budget and keep up with it. If you have an unexpected expense in one area, you should be able to cut back from a different area to cover it if you don’t have enough in savings. When you deplete money from your savings account, prioritize getting that account built back up to where it needs to be.

As with any change you make in life, in order to maintain the motivation required to maintain your new habit, you have to start by identifying your personal “why” for doing it: “For example: ‘I want to become debt-free’ is a good reason to budget. But why do you want to become debt-free? I want to become debt-free so I never have to experience the anxiety and stress of living paycheck to paycheck ever again,” is an even better reason. When you’re looking for your why, don’t stop at the surface layer. Dig deeper”. Identify for yourself why you are starting to budget. What is compelling you now that will continue to propel you moving forward?

Hopefully now you are beginning to see that budgeting doesn’t have to be scary. In fact, it can be quite empowering. Having a budget helps you stay on track to not only covering your monthly expenses but to meeting your long-term financial goals. Take ownership of your finances so that they don’t take ownership of you. By creating a simple budget, choosing a method that works for you, sticking with it, and adjusting as needed, you are well on your way to having a healthy grasp on your finances.

References

- Hayes, Abby. How to Create a Budget That Actually Works. (2018, October 26). Retrieved from https://www.doughroller.net/budgeting/the-idiots-guide-to-creating-a-budget-that-actually-works/ (accessed 2019, September 20).

- Intuit Mint Life. Budgeting 101: How to Create a Budget. (2019, August 19). Retrieved from https://blog.mint.com/budgeting/budgeting-101/ (accessed 2019, September 20).

- Money Management International. Ultimate Guide to Creating a Budget. (2019). Retrieved from https://www.moneymanagement.org/budget-guides/create-a-budget (accessed 2019, September 20).

- O’Shea, Bev and Lauren Schwahn. Budgeting 101: How to Create a Budget. (2019, January 18). Retrieved from https://www.nerdwallet.com/blog/finance/how-to-build-a-budget/ (accessed 2019, September 20).

- Vohwinkle, Jeremy. Make a Personal Budget in 6 Steps: A Step-by-Step Guide to Make a Budget. (2019, March 20). Retrieved from https://www.thebalance.com/how-to-make-a-budget-1289587 (accessed 2019, September 20).